Subaru Corporation: An undervalued pick

A comprehensive view of Subaru Corporation's fundamentals, future business prospects and its company valuation.

Subaru Corporation was founded on July 15th, 1953, under the name “Fuji Heavy Industries” with historical ties to an aircraft manufacturing company during WWII. Today it is a Japanese conglomerate that manufactures automobiles and aircraft vehicles. The Japanese car-manufacturer Toyota owns a roughly 20% stake in Subaru Corporation and produces certain products in a tie up with them. Additionally, it has historically produced military vehicles and continues to do so with some of its revenue generated from its business with the Japanese Defense Agency producing everything from aircrafts to helicopters.

Figure 1: 1958 Subaru 360

In the FY23, 97.7% of Subaru’s revenue was generated from its automobile segment with 2.2% stemming from its aerospace division. The U.S. remains Subaru’s largest market for its automobile sales with 695,000 units sold (71% of total unit sales). The Japanese market is the second largest with 99,000 units sold (10% of total unit sales). Therefore, during this valuation analysis we focus mainly on its automobile segment with respect to the U.S. market. Subaru Corporation today trades at 2,754 JPY with a P/E ratio of 5.5 and a dividend yield of 4%.

Figure 2: Key statistics of Subaru Corporation (Source: TradingView)

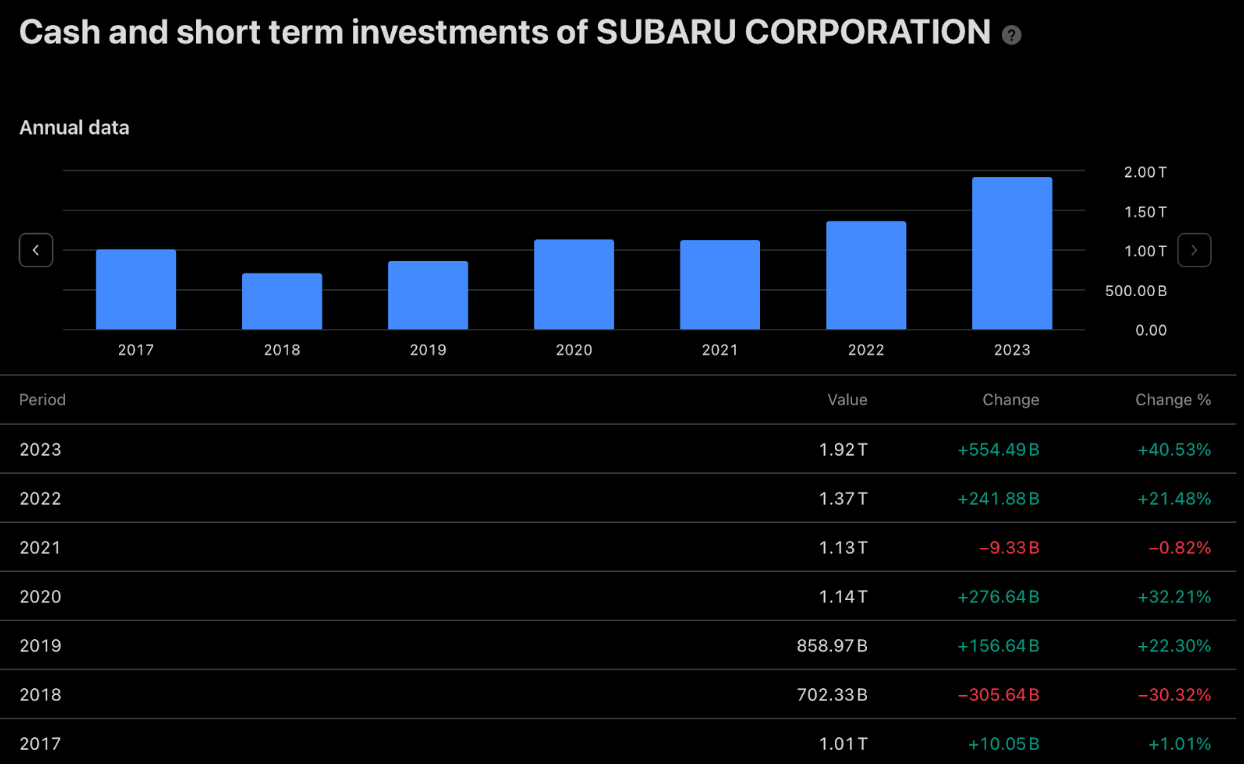

When we view Subaru’s fundamentals, we see that the total debt of Subaru Corporation stands at 523.35 billion JPY as of 2023. However, the cash and short-term investments of Subaru remain at a robust 1.92 trillion JPY. The book value per share of Subaru Corporation stands at roughly 3,400 JPY which is well over the current stock price. Their EPS over the past 7 years has grown at an average pace of 9.5-10% YOY. Given that this growth includes the COVID-19 years, this exhibits a certain level of strength in the business’ earnings. Their return on invested capital stands at 14.2% (granted that it stood at 8.29% pre-pandemic) compared to their reported weighted average cost of capital stands around 6%.

Figure 2: Total debt of Subaru Corporation (Source: TradingView)

Figure 3: Total Cash and short term investments of Subaru Corporation (Source: TradingView)

Figure 4: Earnings per share of Subaru Corporation (Source: TradingView)

Figure 4: Return on invested capital of Subaru Corporation (Source: TradingView)

Despite their performance in the past, the business’ growth prospects in the upcoming decade heavily hinges on its ability to get a foot in the door in the EV (Electric Vehicle) segment. There have been concerns regarding their current lack of a varied line of EV products. The barriers to entry surrounding EV manufacturing remain quite steep with the necessity to repurpose ICE vehicle producing factories, organise battery production, acquire a cheap source of raw materials, and finally outcompete other players in the market while trying to better cater to consumer preferences. Warren Buffet invested in Coca Cola due to the moat that it had with no other beverage company unable to produce its taste or command its brand loyalty at the time. Paired with the financial stability of Coca-Cola, that investment was a no-brainer.

Subaru Corporation possesses the right ingredients to possibly do well in the upcoming decade. They command a modest global market share of 1%. However, it boasts one of the highest rates of brand loyalty in the industry. Most Subaru owners end up switching to other Subaru products. The second ingredient they possess is a partnership with the Japanese company Panasonic Energy to engage in the production of cylindrical automotive lithium-ion batteries and plan to open a plant for the same. They have also tied up with AMD to design circuits for their chip requirements. They have ear-marked 1.5 trillion JPY to invest in their EV push over the next three years which will involve upgrading their current production lines to also manufacture EVs and overtime establish plants that exclusively produce EVs (enabled by their sound financial position and enormous free cash flow). Finally, they propose to put all these pieces (brand loyalty, financial soundness, and EV investments) together by the year 2028-29.

Now, it is important to admit that many things can go awry during this period. With a U.S. president insistent on a policy of isolationism, a highly competitive market and rising borrowing costs, there are many metaphorical spanners waiting to be cast into the works. However, given their robust financial position and brand loyalty, a lot of the aforementioned factors could possibly be dealt with.

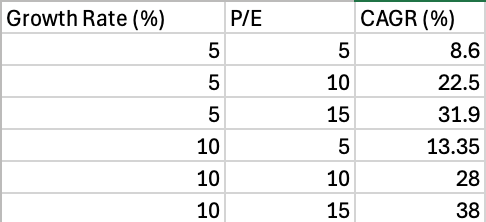

As Howard Marks once said, “no asset is so good that it can’t be overpriced” and “no asset is so bad that there’s not a price at which it’s attractive for purchase”. The reader is free to view Subaru Corporation under the lens of a “good” asset or a “bad” one for it is finally the valuation that remains key. As for the valuation, we use two methods. The first method which is akin to a back of the envelope approximation would be to compound the EPS at different growth rates (5% and 10%), assume a terminal P/E ratio at the end of 5 years (5,10 and 15 as the historical median P/E is 12), and a dividend payout ratio of 20%, calculate the value of the stream of dividends at the end of five years and discount it back to today’s stock price to get at the implied rate of return per year on average. The results are summarised below.

Figure 5: CAGR of Subaru Corporation calculated via method one

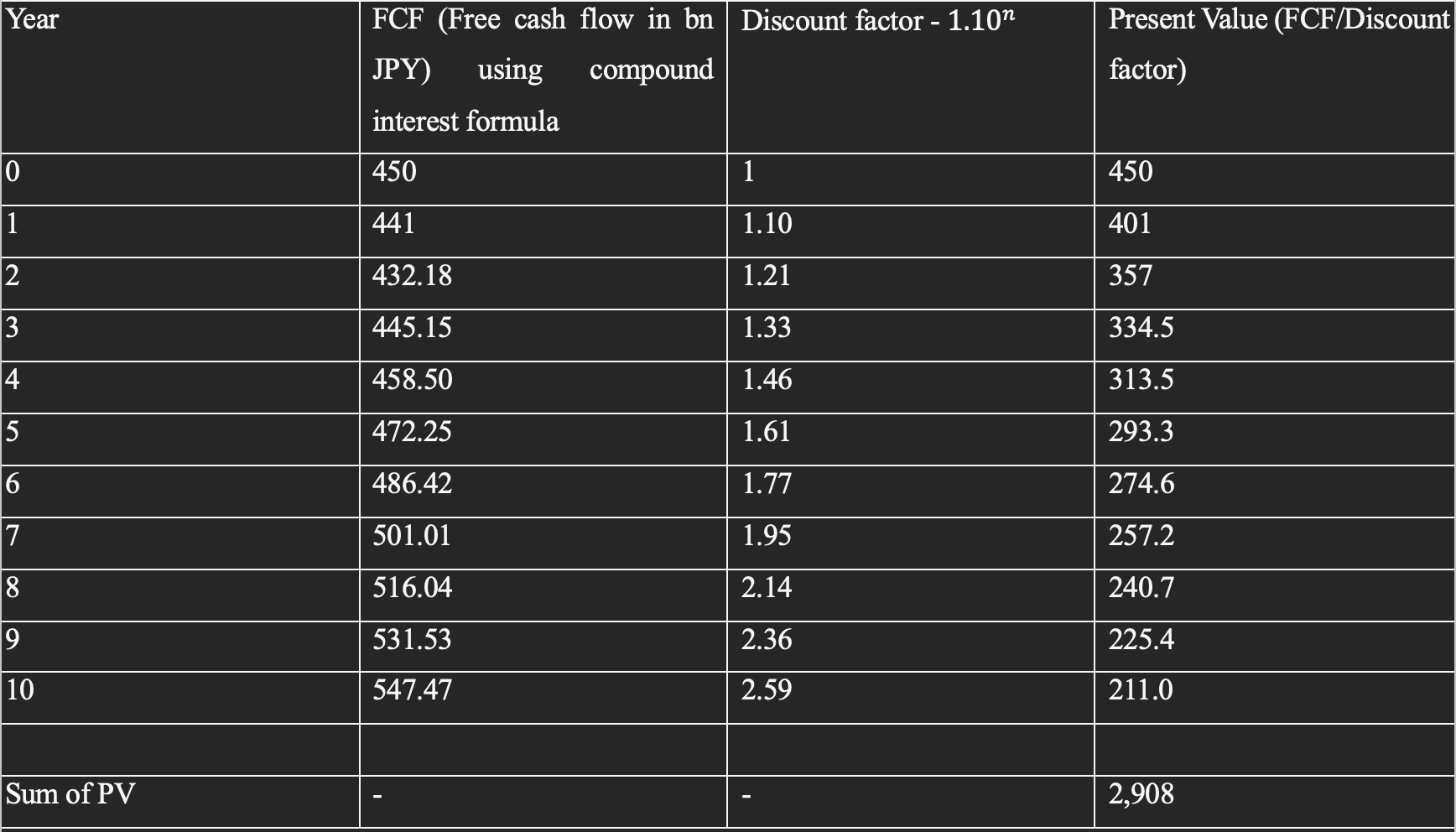

Given that the growth of 5% seems reasonable and a P/E of 10, this method predicts a roughly 22.5% rate of return over the next five years. However, a more rigorous classical DCF method would go as follows. Suppose we conservatively assume that their earnings decline by 2% every year for the next two years, then grow at 3% after that reflecting their EV transition. Also, assuming that their terminal growth rate is 2% to keep up with inflation (the rate at which the company’s free-cash-flow grows in the long run as it matures), and a discount rate (usually the cost of capital + margin of safety) of 10%. A view of the net present value of the company can be calculated as shown below.

Figure 6: Stream of FCF for Subaru Corporation and its present value

Now we calculate the terminal value of the cash flows, with a 2% terminal growth rate and a 10% discount rate using the perpetuity growth formula and divide it with the ten-year discount factor of 2.59 calculated above to give us the PV of the terminal cash flow. Summing up the PV of the free-cash flow of the next ten years and the terminal cash flow value and dividing it by the total number of outstanding shares (751 million) gives us the present value of free cash flow per share which in this case is 7,444 JPY.

A 10% discount rate is conservative, but if we wanted to truly follow the margin of safety approach, we could take an extreme case of a 15% discount rate which through similar calculations as done previously would yield us 4,545 JPY per share. If in the worst case we assumed 0 growth in the FCF with a 2% decline in the first two years and a 15% discount rate, we would still arrive at 4,016 JPY per share. These valuations are very reasonable for a company that is financially sound, commands brand loyalty, and possesses a long-term plan to strategically enter the EV segment. Given these factors, we believe that as of today, Subaru Corporation remains a company that is deeply undervalued and worth considering.

Disclaimer

This Substack does not provide investment advice.

The author is not a SEBI-registered investment advisor.

The content in this article is intended solely for informational and discussion purposes. It is not a recommendation to buy or sell any financial instruments or other products.

Investors should seek personalized advice from their tax, financial, legal, and other advisers regarding the risks and benefits of any transaction before making investment decisions.

The information provided in this article is sourced from generally available information It may be incomplete or summarized.

Investing in financial instruments or other products involves significant risk, including the potential total loss of the invested principal. This article and its author do not claim to identify all the risks or key factors associated with any transaction. The author of this website is not liable for any loss (whether direct, indirect, or consequential) that may result from the use of the information contained in or derived from this website.

Good one Shashwat! It is a good buy and agree with your views

hi shaswat, SUBARU seems to be listed as unsponsored ADR( FUJHY) in the US. do you see a risk for retail investor buying it? or any other option?