Safety in a ‘champion’ index

Safety in a ‘champion’ index

Banks and Why They Matter: An investor's guide to Outperforming the market

(This article was authored by Anand Srinivasan and Sashwath Swaminathan and published in The Hindu newspaper on September 19th 2021).

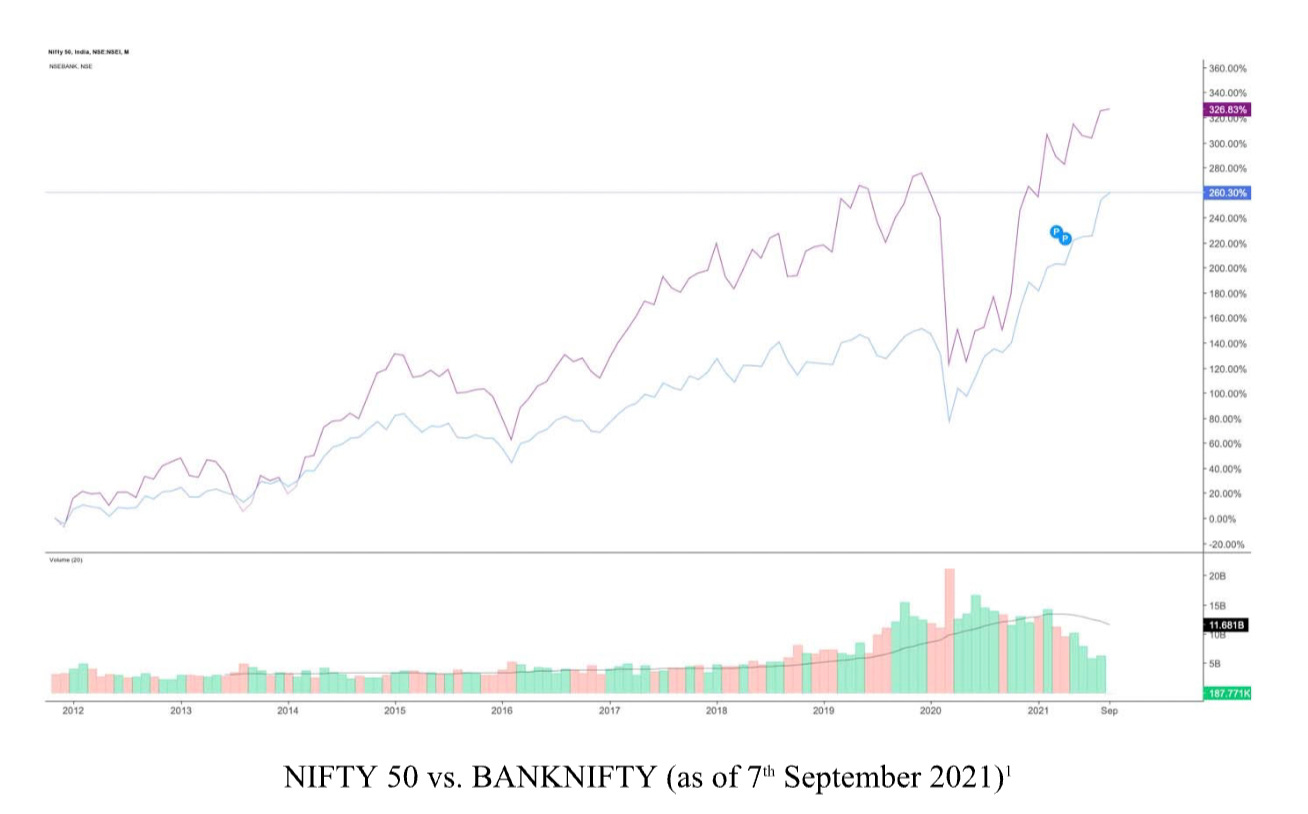

When investing in Indian stocks, names such as TCS, HUL, Britannia, Nestle and ITC constantly provoke interest. However, interestingly, over the last decade, neither the FMCG industry nor the IT sector has outperformed the Nifty 50 index, but rather the banking sector. The accompanying graph shows that the Nifty Bank index has predominantly outpaced the Nifty 50 since 2008.

According to the RBI, the number of scheduled commercial Indian banks includes 22 private sector banks, 11 small finance banks, and 12 public sector banks. In stark contrast, the U.S. has only one-third of our population and has 2,108 banks. Additionally, it should be noted that the top five banks in India dominate the share of the total deposits and transactions.

Concentration risk

The concentration of significant market share in the hands of a few leads to behaviour where independent firms may likely act in cohesion to ensure profit maximisation. A significant barrier to entry into the industry further spurs such behaviour.

The RBI has meticulous rules and is very conservative in distributing large-scale commercial banking licences, as seen by the sparse number of banks. These large banks also keep the financial system in order by lending to and borrowing from each other.

Therefore, as American economist Irving Fisher said, the collapse of even a single bank would wreak havoc on the financial system, as has been observed in the U.S. on multiple occasions. The RBI is aware of this and will go to great lengths to ensure no bank collapses, leading to an added layer of safety for banks as investments. If one may recall the Yes Bank fiasco, the bailout of a troubled bank has been exhibited with great certainty.

Among the several advantages that banks enjoy, the most significant is the access to big finance from their banking peers and from the RBI, which acts as the lender of the last resort.

‘Low-risk bets’

This places banks in a unique position to receive cheap capital, as most asset books are liquid and considered low risk. They have access to low-cost capital through the ability to open current accounts and savings accounts. Fractional reserve banking — in which only a fraction of bank deposits are backed by cash on hand and available for withdrawal to help expand the economy by freeing capital for lending — also allows them to create money temporarily.

It’s not just the markets that recognise banks’ dominance but also NBFCs that want to enter the arena due to the superior benefit of access to low-cost capital. Capital First, an NBFC, merged with IDFC Bank to create the merged entity IDFC First Bank on December 18, 2018.

At the time of the merger, their loan book was ₹1.03 lakh crore. Capital First effectively gained access to low-cost capital to further supplement its existing retail client base. This was also a way for it to circumvent the need to possess a banking licence. There is also word in the wind of another NBFC following this path — Clix Capital is said to be in talks with Suryoday Small Finance Bank to eventually join this elite group of banks, highlighting the attraction the sector holds for aspirants. The graph comparison understates the dominance of banks because the Nifty 50 also consists of banking stocks. This means that the performance of banks has beaten the general market by a far more significant margin than is evident. This also highlights an important point — the market favours businesses with a steady cash flow stream in the long run.

Nonetheless, it is prudent to understand that the banking business is resilient but not immune to threats. This banding together of entities in the banking system can end in the future for many reasons, the principal one being innovative and cutting-edge fintech companies making significant inroads into India.

U.S. scenario different

Small finance banks, which offer far more competitive rates, also bring competition and healthy behaviour to the table. The eventual and much-needed liberalisation of the banking sector might also end the dream run. The U.S. has liberalised its banking sector immensely, resulting in many players in the game there. Although most of the market share still belongs to the 10 largest banks, it is clear from the market performance that the banking sector (which underperformed the S&P 500) is nowhere as dominant as it is in India. Regardless of these threats, at least for the time being, banks will continue to enjoy advantages that no other industry can.

Disclaimer

This Substack does not provide investment advice.

The content in this article is intended solely for informational and discussion purposes. It is not a recommendation to buy or sell any financial instruments or other products.

Investors should seek personalized advice from their own tax, financial, legal, and other advisers regarding the risks and benefits of any transaction before making investment decisions.

The information provided in this article is sourced from generally available information and, while believed to be reliable, its accuracy and completeness cannot be guaranteed. It may be incomplete or summarized.

Investing in financial instruments or other products involves significant risk, including the potential total loss of the invested principal. This article and its author do not claim to identify all the risks or key factors associated with any transaction. The author of this website is not liable for any loss (whether direct, indirect, or consequential) that may result from the use of the information contained in or derived from this website.

Isn’t it a cycle? As interest rates come down, banks should see sectoral rotations

great article!