Navigating Economic Shifts: Strategic Investment Insights for Mid-2024

Navigating Economic Shifts: Strategic Investment Insights for Mid-2024

Harnessing Treasury Yields and Uncovering Stock Market Bargains in a Cooling Economy

As we enter the second half of 2024, stopping and taking stock of the current economic situation is vital for those interested in global markets such as the United States. As of 1st July 2024, the U.S. interest rate stands at 5.5%, higher than in the past 20 years (refer to Fig below).

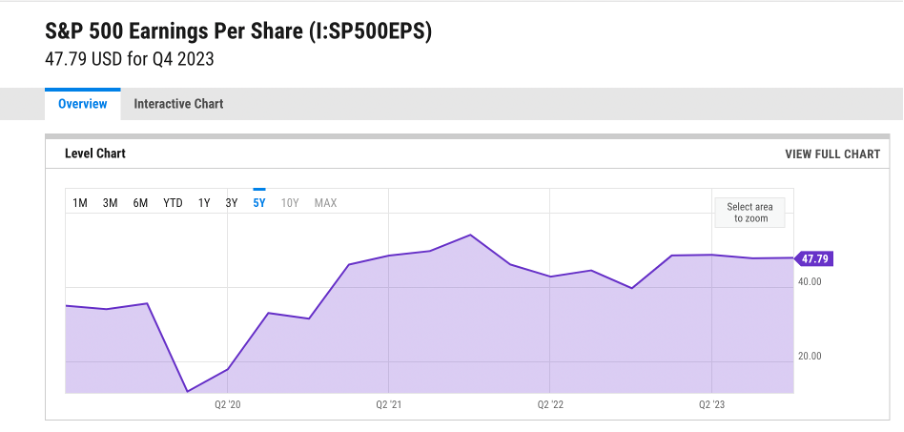

The U.S. inflation rate stands at 3.72%, well below its peak in 2022, where it previously stood at 9.1% (refer to Fig below). As the U.S. economy cools down, evidenced by the lack of growth in earnings per share over the past three years, it seems increasingly likely that the Federal Reserve would not seek to raise rates further but might slash rates sometime this or next year.

What this means for us as investors is that when the interest rate is cut, we should see an appreciation in the trading value of U.S. treasury bills. U.S. T-Bills represent money that the U.S. government borrowed from the bill holder. Therefore, the individual is entitled to a fixed payment based on the bond's face value. Suppose you were to lend the U.S. government 100 dollars for ten years with a coupon rate of 10%; this would imply that each year, you would receive a fixed sum of 10 dollars and be paid the entire principal of 100 dollars at the end of 10 years. Interest rates can be viewed as the cost of money. Therefore, when the interest rate is lower, the government can now finance their borrowings at a lower cost with multiple individuals willing to lend money to them for a lower rate. Thus, in such a scenario, the price of your T-Bill in the financial market will appreciate to match this lower cost of borrowing. Continuing with the previous example, suppose the interest rate in the U.S. falls to 6%. For the sake of this exercise, let us assume the government issues new T-Bills at the same coupon rate. Your T-Bill's value will now appreciate to around 129.4 dollars due to the lower interest rate (a detailed run-through of the calculation can be made available based on demand). As seen below, the current U.S. 5-year treasury yield stands at 4.43%, higher than we have seen for over 16 years. With the historical average rate of inflation in the U.S. standing at 3.3%, the holder of the 5-year treasury would gain roughly 1.1% year on year and even more if the economy were to slow down further, leading to a further drop in the inflation rate.

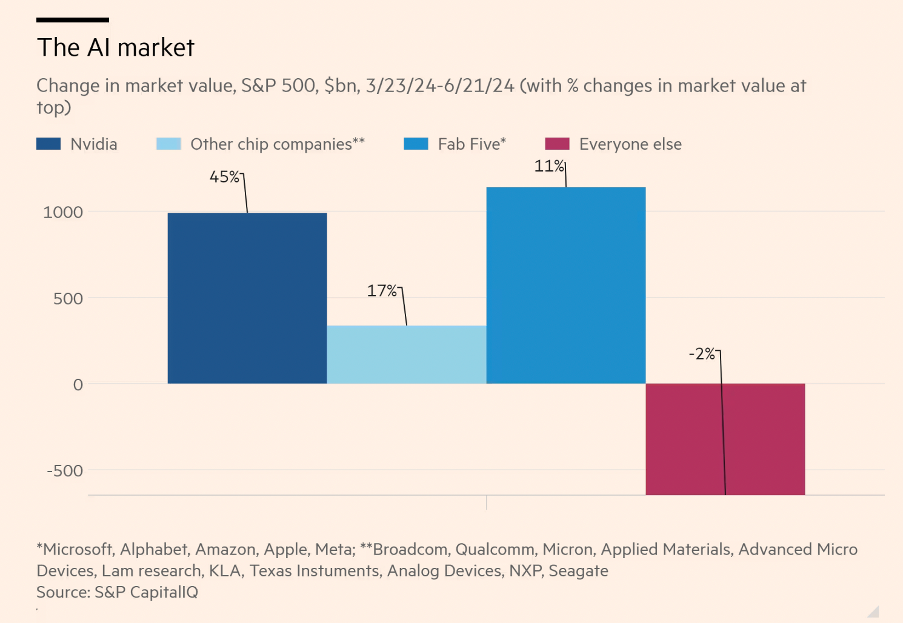

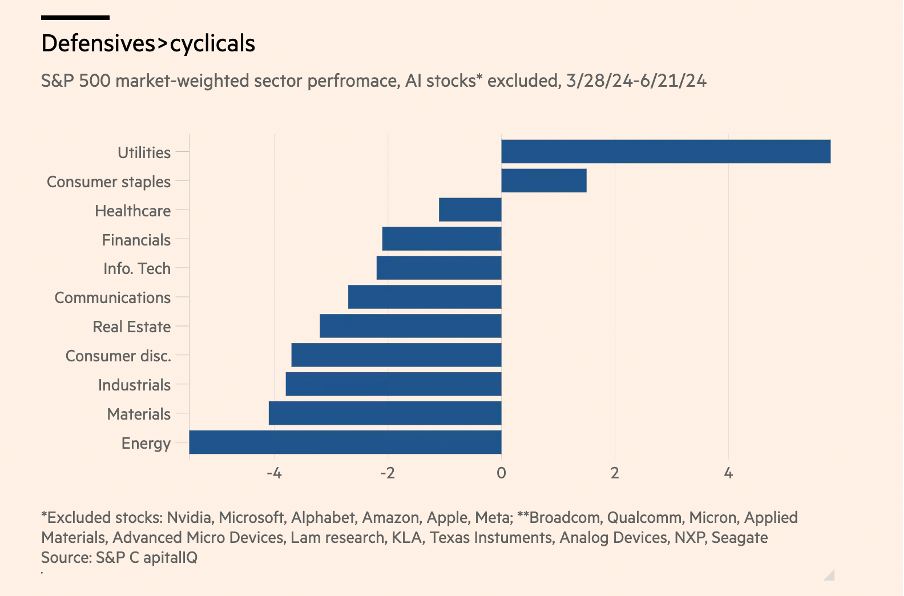

In contrast, a surface-level analysis indicates that retail investors would receive a dividend yield of 1.3% by investing in the S&P500 and not receive much in the way of price appreciation due to the slowing down of the U.S. economy, which is also signalled by the stagnating earnings per share of the S&P500. A closer look indicates that, in reality, most of the index is declining. Most of the gains made by the index come from the magnificent seven companies, including Apple, Microsoft, Nvidia, Meta, Alphabet, Amazon and Tesla. As shown in the figure below, Nvidia alone makes up for a large portion of the S&P500's gain over the past two years. Moreover, a closer look at the sectoral breakdown indicates a vastly gloomy picture for the S&P500, with most sectors declining by over 2% or more.

Furthermore, the actual performance of the S&P500 since the year 2021 can be understood by the S&P500 equal weights index, which keeps the weights of its constituents the same. Here, we see that despite the gain in market value by the magnificent seven companies, the broader index has seldom posted a gain. In fact, if one were to isolate the gains made by A.I. stocks, the more extensive index would drop considerably.

A 6.93% absolute gain over three years would translate to an annual rate of return of 2.25% over the three years. The inflation rate over this period has staunchly remained above 5%, only falling to the 3% range in the latter half of the previous year. This means that without A.I. stocks inflating performance, the index would have done extremely poorly in comparison to the rate of inflation.

Today, it makes prudent sense to accumulate treasury bonds at higher yields and benefit from the possibly soon-to-be declining interest rate. Additionally, we believe that the general underperformance of the S&P500 index, apart from the magnificent seven companies, opens up opportunities to start looking at bargain buys of companies trading below their intrinsic value in the U.S. market. A more significant concentration in treasuries with some exposure to the stock market seems to be the most prudent way for the investor to navigate current global market conditions.

Disclaimer

This Substack does not provide investment advice.

The content in this article is intended solely for informational and discussion purposes. It is not a recommendation to buy or sell any financial instruments or other products.

Investors should seek personalized advice from their tax, financial, legal, and other advisers regarding the risks and benefits of any transaction before making investment decisions.

The information provided in this article is sourced from generally available information It may be incomplete or summarized.

Investing in financial instruments or other products involves significant risk, including the potential total loss of the invested principal. This article and its author do not claim to identify all the risks or key factors associated with any transaction. The author of this website is not liable for any loss (whether direct, indirect, or consequential) that may result from the use of the information contained in or derived from this website.

Good insights please post the detailed Calculation on how interest rate will have impact on Bond price

Amazing article! Can you please demonstrate how the Treasury bills appreciate ??? Would be nice to see a detailed explanation (as you have mentioned it can be done in demand). Thank you